Vlad Zghurskyi

01.04.2026

10 Min Read

TL;DR

Defense technology activity in Q4 2025 focused on the rapid expansion of autonomous systems, electronic warfare technologies, and AI-driven battlefield software. Companies such as Shield AI, Anduril, and General Atomics are increasingly acquiring niche technology providers to accelerate development of systems capable of operating in contested environments. At the same time, battlefield data (particularly from modern conflicts) is becoming a critical competitive advantage, shaping both valuation premiums and acquisition strategies in the defense technology ecosystem.

Mini Glossary

Electronic Warfare (EW)

Technologies used to disrupt or manipulate enemy communications, radar systems, and electronic signals.

SIGINT (Signals Intelligence)

Intelligence collected through interception and analysis of electronic communications and signals.

GPS-Denied Environment

Operational conditions where satellite navigation signals are unavailable or intentionally jammed.

Edge AI

Artificial intelligence systems capable of processing data locally on devices such as drones or robots without relying on cloud connectivity.

Replicator Program

A U.S. Department of Defense initiative aimed at rapidly deploying autonomous systems and drone swarms at scale

Key Signals & Deals

Signals Rationale

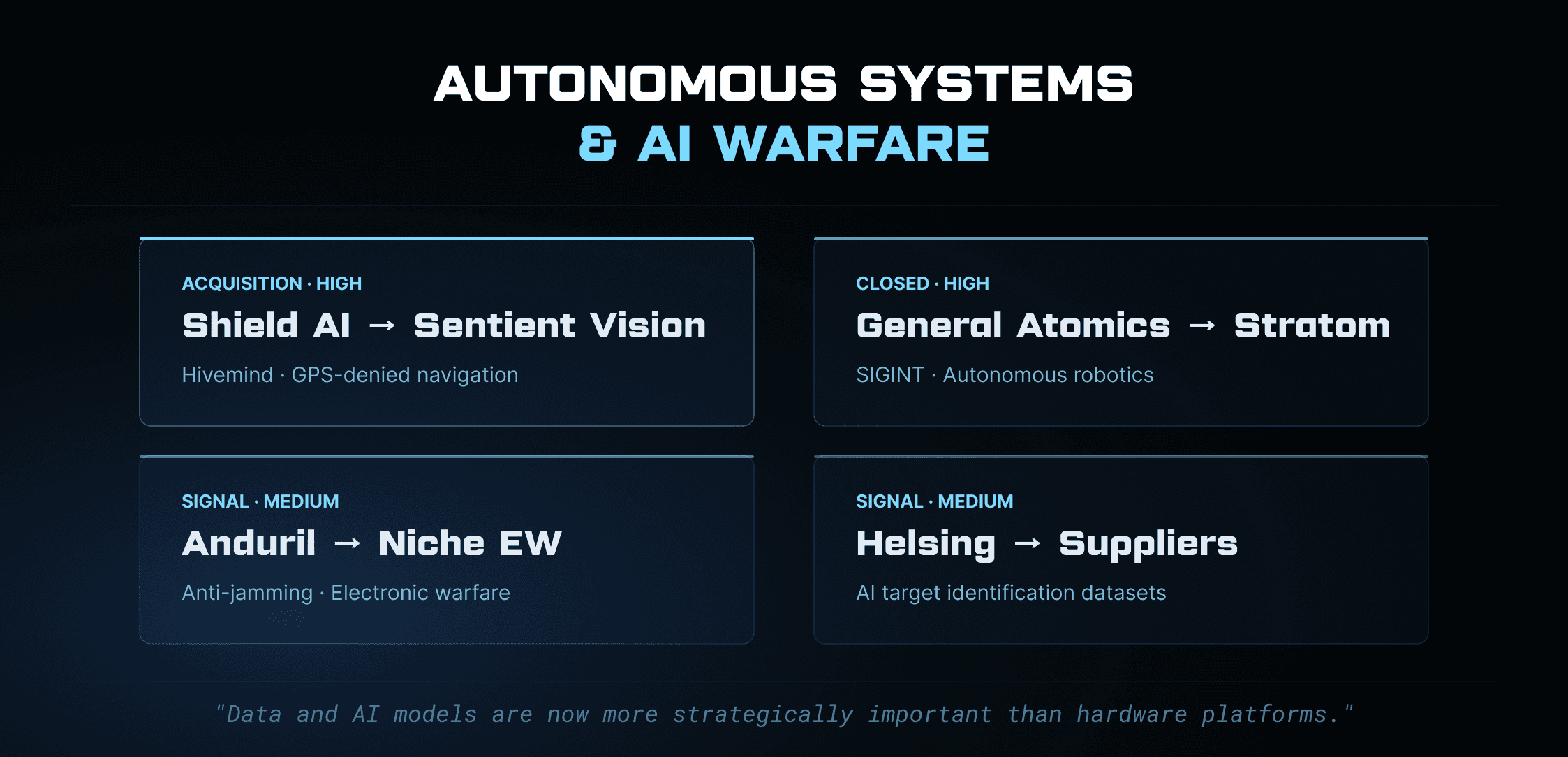

The Shield AI acquisition of Sentient Vision strengthens its Hivemind autonomous flight platform, integrating visual navigation technologies that allow drones to operate effectively in GPS-denied environments. These capabilities have been validated in real-world combat scenarios.

General Atomics’ acquisition of Stratom reflects a broader shift from purely hardware-based drone platforms toward software-defined intelligence systems, particularly in signals intelligence and autonomous robotics.

Meanwhile, Anduril’s acquisition signals in electronic warfare suggest a strategic push toward anti-jamming technologies capable of operating in environments with heavy electronic interference.

The signals around Helsing’s supplier acquisitions point to efforts to expand datasets used for AI-based target identification, which is becoming a critical capability in modern defense operations.

Sector Trends

Electronic Warfare Data as Strategic Assets

Electronic warfare signal libraries are rapidly becoming valuable resources for training defense AI systems.

Edge AI Deployment

Autonomous platforms increasingly rely on onboard AI processing, allowing drones and robotic systems to operate without constant remote control.

Autonomous Systems Expansion

Programs such as the U.S. Replicator initiative are accelerating the development and deployment of low-cost autonomous platforms.

Dual-Use Interpretation

Many technologies involved in defense acquisitions also have civilian applications.

Visual navigation systems originally developed for autonomous vehicles can be adapted for military drone navigation in GPS-denied environments. Similarly, machine learning models designed for industrial robotics can be repurposed for autonomous military platforms.

Another key factor is the transfer of operational data. Combat-tested datasets significantly improve the training of AI systems, giving companies with access to real-world operational data a competitive advantage.

Structured Signals

Signal Card | Description | Context | Confidence |

Anduril EW Niche | Anti-jamming acquisitions | Replicator program expansion | Medium |

DIU UUV Push | Underwater autonomy startups | Pacific theater preparation | High |

Analyst Thesis

The defense technology sector is transitioning toward software-defined military systems, where data and AI models are more strategically important than traditional hardware platforms.

Electronic warfare datasets and battlefield signal libraries are emerging as critical training resources for defense AI systems, effectively becoming strategic assets comparable to energy resources.

At the same time, the ability to update software systems rapidly, sometimes within 48-hour operational cycles, is enabling defense technologies to evolve faster than traditional hardware procurement cycles.

Companies capable of integrating autonomous systems, electronic warfare capabilities, and AI analytics platforms are likely to dominate the next phase of defense technology development.

Sources Hierarchy

Tier 1 — Primary Sources

Defense contractor announcements, government procurement documentation, regulatory filings.

Tier 2 — Financial Media

Reuters, Bloomberg, Financial Times.

Tier 3 — Defense Industry Research

Defense News, SIPRI, venture capital and aerospace industry databases.

Confidence Framework

High Confidence

Confirmed acquisitions and officially disclosed transactions.

Medium Confidence

Signals supported by multiple industry reports but not fully confirmed.

Low Confidence Early-stage signals or speculative developments.

FAQ

Why are autonomous systems attracting defense investments?

Autonomous drones and robotic systems reduce operational risk and allow military forces to operate effectively in contested environments.

What makes electronic warfare data valuable?

Electronic warfare datasets help train AI systems to detect and counter enemy communication and radar signals.

Why are defense technologies increasingly software-focused?

Software systems can be updated quickly, allowing military platforms to adapt faster than traditional hardware development cycles.