Vlad Zghurskyi

01.04.2026

10 Min Read

TL;DR

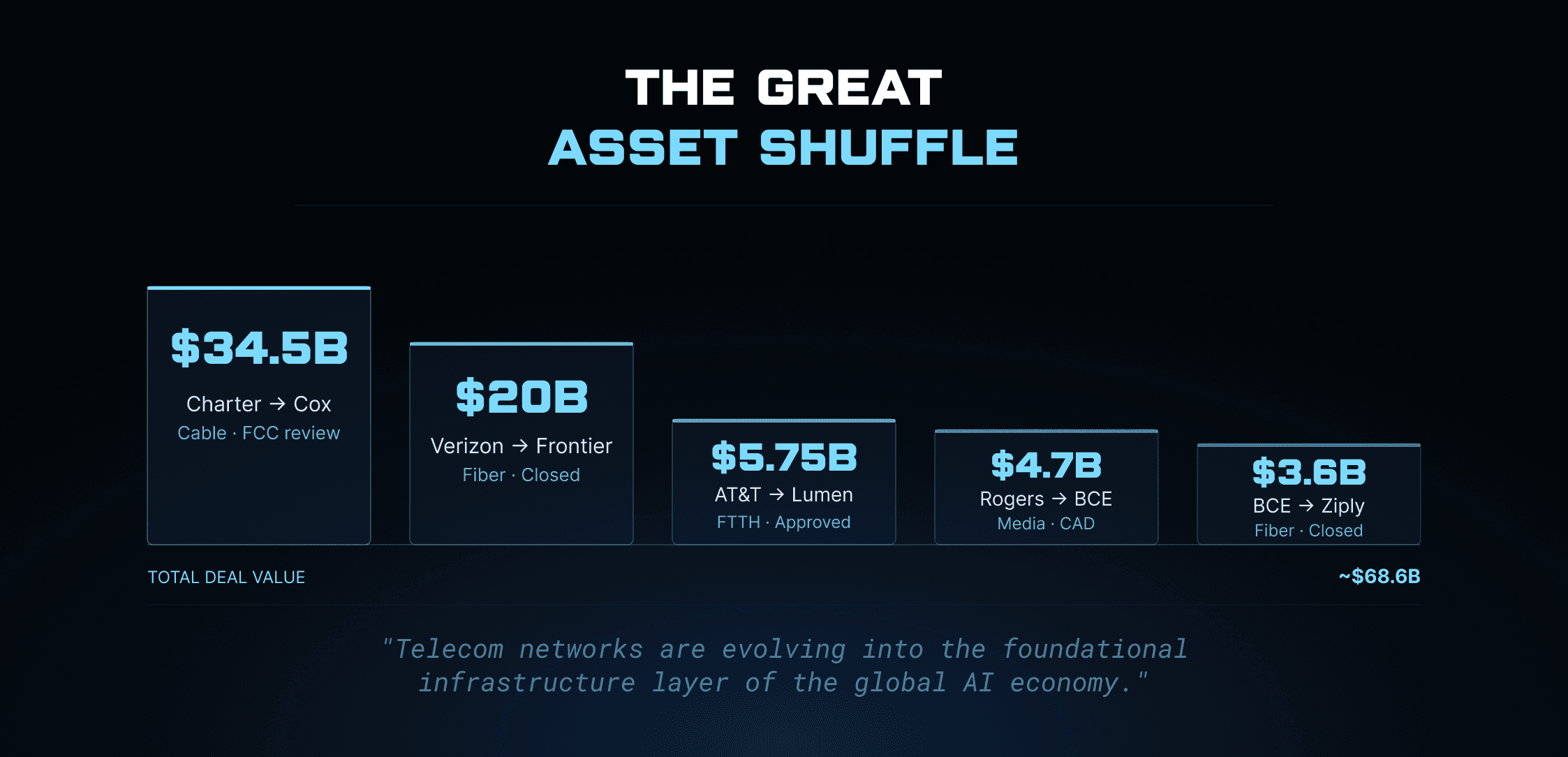

Telecom M&A in North America during Q4 2025 was defined by a large-scale “Great Asset Shuffle” in fiber infrastructure and AI network backbones. Major transactions such as Verizon’s $20B acquisition of Frontier and AT&T’s $5.75B purchase of Lumen’s consumer fiber assets highlight the industry's shift toward fiber networks capable of supporting AI data traffic and future 6G infrastructure. Canadian operators also increased cross-border investment, while telecom providers repositioned themselves as core infrastructure providers for AI computing and cloud services.

Mini Glossary

FTTH (Fiber to the Home)

Broadband infrastructure delivering fiber-optic connectivity directly to residential buildings.

FWA (Fixed Wireless Access)

Wireless broadband delivered through cellular infrastructure instead of wired fiber connections.

Backbone Network

High-capacity infrastructure that carries large volumes of internet traffic between regions and data centers.

QKD (Quantum Key Distribution)

A secure communication technology using quantum mechanics to protect encryption keys.

BEAD Program

A $42.5B U.S. federal initiative designed to expand broadband infrastructure in underserved regions.

Key Deals

Deal Rationale

Fiber infrastructure has become the central strategic asset in telecom consolidation.

The Charter–Cox transaction represents one of the largest potential cable consolidations in the U.S., aimed at scaling broadband networks and defending market share against 5G fixed wireless access providers. Analysts estimate potential operational synergies of approximately $500M annually.

AT&T’s acquisition of Lumen’s consumer fiber business supports the company’s long-term strategy to expand fiber connectivity to 60 million U.S. homes by 2030.

Meanwhile, Verizon’s Frontier acquisition adds a major backbone network of approximately 350,000 miles of fiber infrastructure, supporting future 6G networks and edge computing infrastructure.

Canadian operators are also expanding their presence in the U.S. market. BCE’s acquisition of Ziply Fiber strengthens its position in the Pacific Northwest, while Rogers’ purchase of BCE’s MLSE sports stake reflects a strategic pivot toward premium media content.

Market Trends

Last-Mile Competition

Cable, fiber, and fixed wireless access are competing for control over last-mile broadband connectivity.

Capital Arbitrage

Canadian telecom companies increasingly invest in U.S. fiber networks due to stronger growth opportunities and regulatory flexibility.

Asset-Light Strategies

Companies such as Lumen are transitioning away from consumer networks toward AI backbone infrastructure, supported by contracts with hyperscale cloud providers.

Structured Signals

Signal Card | Description | Context | Confidence |

Private 5G PE | Blackstone / KKR fiber rollups | Amazon and Walmart warehouse networks | Medium |

Lumen AI Pivot | $5B Microsoft / Google backbone contracts | Enterprise AI infrastructure | High |

SES / Intelsat DoD | Multi-orbit satellite networks vs Starlink | Government communications contracts | High |

Analyst Thesis

Competition for last-mile connectivity is intensifying between cable networks, fiber infrastructure, and fixed wireless access technologies.

The BEAD broadband program ($42.5B) is acting as a major catalyst for telecom M&A activity by subsidizing infrastructure expansion across underserved regions.

Meanwhile, telecom companies are increasingly repositioning themselves as AI infrastructure providers, supplying the backbone networks that connect hyperscale data centers and cloud platforms.

Technologies such as quantum key distribution (QKD) are also gaining attention as telecom operators prepare for future cybersecurity risks, including the “store now, decrypt later” threat model.

Overall, telecom networks are gradually evolving into the foundational infrastructure layer supporting the global AI economy.

Sources Hierarchy

Tier 1 — Primary Sources

Corporate announcements, regulatory filings, FCC documentation.

Tier 2 — Financial Media

Reuters, Bloomberg, Financial Times.

Tier 3 — Industry Research

Telecom market analysis, infrastructure investment reports, venture capital databases.

Confidence Framework

High Confidence

Confirmed deals and officially disclosed transactions.

Medium Confidence

Deals currently under regulatory review or widely reported by financial media.

Low Confidence

Early-stage signals or market speculation.

FAQ

What drove telecom M&A activity in North America during Q4 2025?

The primary drivers were fiber infrastructure expansion, broadband competition, and the growing importance of AI network backbones.

Why are telecom companies investing heavily in fiber networks?

Fiber provides the bandwidth and reliability needed to support cloud computing, AI workloads, and next-generation mobile networks.

How does the BEAD program influence telecom deals?

The $42.5B federal broadband initiative incentivizes companies to expand infrastructure into underserved regions, increasing acquisition activity.