Vlad Zghurskyi

01.04.2026

10 Min Read

TL;DR

Technology M&A activity in Q4 2025 focused heavily on AI infrastructure, semiconductor financing, and cloud computing capacity. Strategic investments by companies such as Nvidia, Microsoft, and Intel demonstrate how the industry is rapidly consolidating around the infrastructure required to support large-scale AI workloads. Deals increasingly combine hardware, data infrastructure, and cloud computing, while access to energy resources and semiconductor manufacturing capacity is becoming a decisive factor in future technology expansion.

Mini Glossary

GPU Cloud

Cloud infrastructure designed specifically for large-scale AI computation using graphics processing units.

Semiconductor Foundry

Manufacturing facilities where semiconductor chips are produced for technology companies.

RAG (Retrieval-Augmented Generation)

An AI architecture that combines language models with external data sources to improve response accuracy.

Hyperscalers

Large cloud computing providers such as Amazon, Microsoft, and Google that operate massive global data center infrastructure.

Power-to-Compute

A concept referring to the growing importance of energy infrastructure in enabling large-scale AI computation.

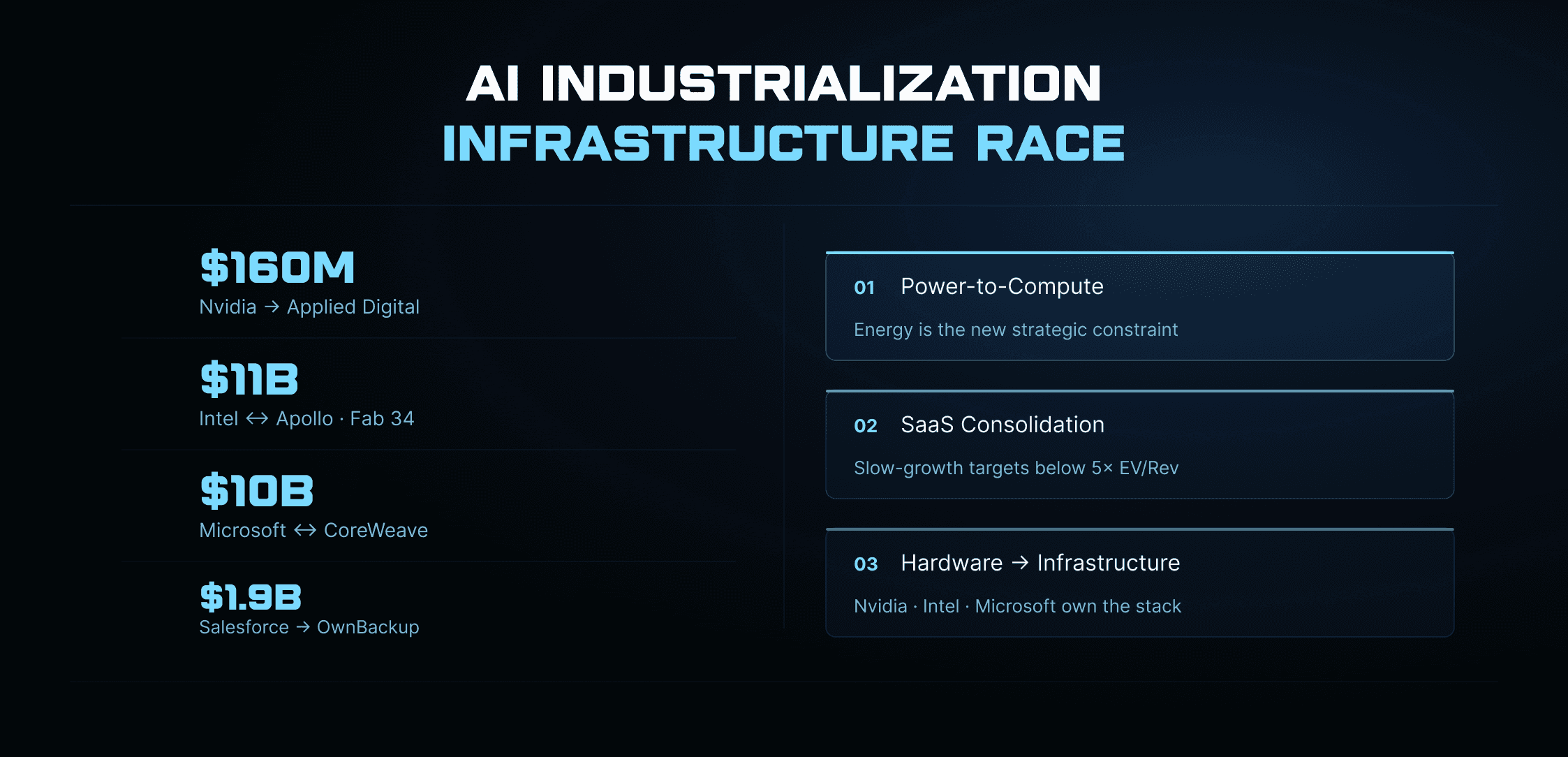

Key Deals

Deal Rationale

Technology M&A in North America is increasingly focused on controlling the full AI infrastructure stack.

Nvidia’s investment in Applied Digital reflects its strategy of vertically integrating cloud infrastructure around its next-generation Blackwell and Rubin GPU architectures, ensuring demand for its hardware platforms.

The Intel–Apollo partnership represents a new financial model for semiconductor manufacturing. By involving private capital, Intel can expand production capacity while reducing the financial burden of building advanced fabrication facilities.

Salesforce’s acquisition of OwnBackup strengthens the reliability of enterprise data pipelines used by AI agents. Clean and well-structured datasets are essential for technologies such as retrieval-augmented generation systems.

Finally, Microsoft’s financing of CoreWeave highlights the rapid growth of specialized GPU cloud providers that support large-scale AI model training and inference workloads.

Market Trends

Power-to-Compute Economy

Energy infrastructure is becoming a central component of technology expansion as AI workloads dramatically increase electricity demand.

SaaS Market Consolidation

Software companies with slower growth rates are increasingly becoming acquisition targets as valuations drop below 5× EV/Revenue multiples.

Talent Migration

Canada’s technology hubs, particularly Toronto and Montreal, are experiencing talent outflows to U.S. companies offering higher compensation and larger AI research budgets.

Structured Signals

Signal Card | Description | Context | Confidence |

Google Wiz Retry | $23B potential acquisition attempt | Cloud security consolidation | Low |

AWS Talen Nuclear | $650M nuclear-powered data center | Power-to-compute infrastructure | Medium |

Analyst Thesis

The North American technology sector is entering a phase of AI industrialization, where the primary competitive advantage lies in controlling the infrastructure required to train and operate AI systems.

Hardware companies are transforming into infrastructure owners, while software companies increasingly focus on data governance and security.

At the same time, energy supply is becoming a strategic constraint. Data center operators are exploring long-term power contracts and alternative energy sources, including nuclear power, to support future AI workloads.

This convergence between energy, semiconductors, and cloud computing suggests that future technology M&A will increasingly involve cross-sector partnerships between infrastructure providers, cloud platforms, and energy companies.

Sources Hierarchy

Tier 1 — Primary Sources

Corporate announcements, investor presentations, regulatory filings.

Tier 2 — Financial Media

Reuters, Bloomberg, Financial Times.

Tier 3 — Industry Research

Technology market reports, venture capital databases, semiconductor industry analysis.

Confidence Framework

High Confidence

Confirmed deals or officially announced investments.

Medium Confidence

Widely reported transactions supported by multiple credible sources.

Low Confidence Preliminary discussions or market speculation.

FAQ

Why is AI infrastructure driving technology M&A?

AI systems require massive computing power, specialized chips, and cloud infrastructure, encouraging companies to acquire or partner with infrastructure providers.

Why are semiconductor investments increasing?

Chip manufacturing capacity is limited globally, making semiconductor production a strategic priority for technology companies.

How does energy influence the technology sector?

AI data centers consume enormous amounts of electricity, making reliable energy supply a critical factor in future expansion.