Vlad Zghurskyi

01.04.2026

10 Min Read

TL;DR

Media M&A activity in Q4 2025 focused on IP consolidation and the transition toward AI-generated content production. The potential Netflix acquisition of Warner Bros. Discovery’s studios and Max streaming platform would represent one of the largest media consolidations in recent history. At the same time, companies such as Disney are integrating generative AI technologies into content pipelines, while strategic investments in sports streaming platforms highlight the continued value of live content as the last stable audience anchor in the streaming era.

Mini Glossary

IP (Intellectual Property)

Media franchises and story universes that can be monetized across films, TV, games, and merchandise.

DTC (Direct-to-Consumer)

Streaming platforms that distribute content directly to viewers without cable networks.

Generative AI Content

Media assets created or enhanced using generative AI tools such as video generation models.

C2PA Standard

A digital content authentication framework designed to verify the origin of media and prevent deepfakes.

Content Aggregation The bundling of multiple streaming or broadcast sources into a single distribution platform.

Key Deals

Deal Rationale

Media consolidation is increasingly driven by the value of large intellectual property libraries.

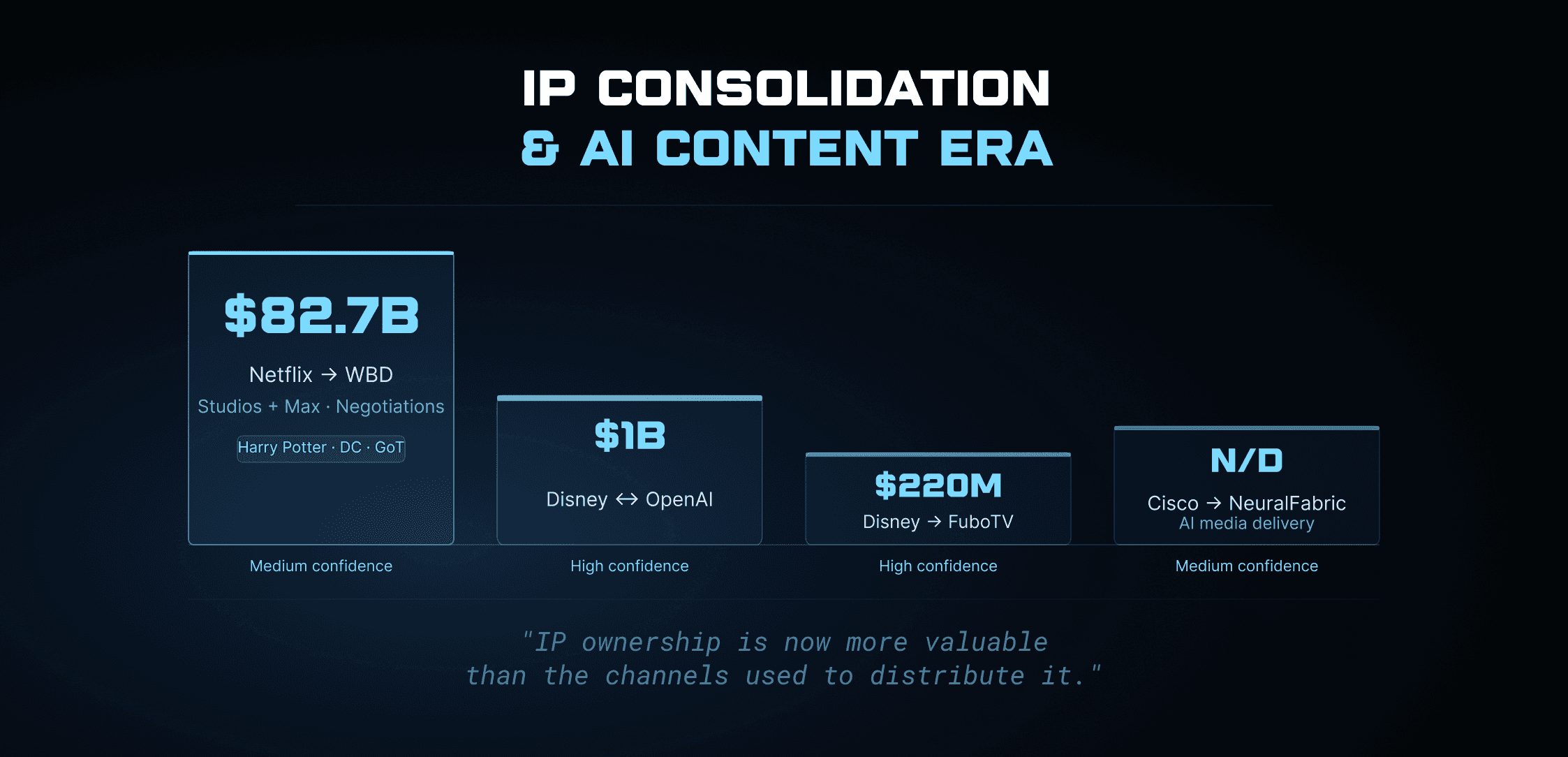

The potential Netflix–Warner Bros. Discovery transaction would allow Netflix to control some of the most valuable franchises in entertainment, including Harry Potter, DC, and Game of Thrones. At the same time, legacy linear television assets such as CNN and Discovery channels may be separated into a new spin-off structure.

The Disney–OpenAI partnership signals the arrival of generative AI within mainstream media production. Licensing franchises such as Marvel and Star Wars for AI-generated storytelling could reduce production costs by 30–40% while accelerating content output.

Meanwhile, Disney’s investment in FuboTV reflects the growing strategic importance of sports aggregation ahead of the launch of ESPN’s direct-to-consumer streaming platform.

Finally, Cisco’s acquisition of NeuralFabric targets infrastructure improvements needed to manage AI-generated media traffic and ultra-high-definition streaming formats such as 8K video.

Market Trends

Deconglomeration of Media Giants

Large media conglomerates are separating traditional television businesses from streaming and content production operations.

AI-Native Content Production

Studios are beginning to integrate generative AI into content pipelines, allowing faster script development, visual effects production, and digital asset generation.

Sports as the Last Live Content Anchor

Live sports remain one of the few types of content that consistently attracts real-time audiences, making sports streaming platforms strategic assets.

Structured Signals

Signal Card | Description | Context | Confidence |

Skydance WBD | $108.4B hostile bid rejected | Oracle-backed studio modernization strategy | High |

Cisco NeuralFabric | AI 8K delivery + deepfake detection | Media infrastructure security | Medium |

Analyst Thesis

The North American media industry is shifting from distribution dominance toward intellectual property ownership.

As streaming platforms mature, the ability to control major entertainment franchises becomes more valuable than the channels used to distribute them. This explains why consolidation efforts increasingly focus on acquiring content libraries rather than distribution networks.

Generative AI technologies are also beginning to transform production workflows. Integration of tools like Sora-style video generation could reduce production costs by 30–40%, while allowing studios to scale content creation more efficiently.

However, despite rapid innovation in digital media, live sports remain the most defensible content category. As a result, sports streaming platforms and rights agreements will likely remain central to future M&A strategies.

Regulatory scrutiny is also increasing. U.S. authorities are closely monitoring large-scale consolidation deals such as Netflix–Warner Bros. Discovery, partly due to concerns about market dominance relative to user-generated content platforms.

Sources Hierarchy

Tier 1 — Primary Sources

Corporate announcements, investor presentations, regulatory filings.

Tier 2 — Financial Media

Bloomberg, Reuters, Financial Times.

Tier 3 — Industry Research

Entertainment market reports, streaming analytics platforms, venture capital databases.

Confidence Framework

High Confidence

Confirmed transactions or officially announced partnerships.

Medium Confidence

Deals reported by reputable financial media but still under negotiation.

Low Confidence Early-stage market signals or strategic rumors.

FAQ

Why are media companies focusing on IP ownership?

Major franchises allow studios to generate revenue across films, series, games, and merchandise, making them highly valuable long-term assets.

How is AI affecting the media industry?

Generative AI tools are enabling faster and cheaper content production, potentially reducing costs by up to 40%.

Why are sports platforms important for media companies?

Live sports content consistently attracts real-time audiences, making it one of the few stable drivers of streaming subscriptions.