Vlad Zghurskyi

01.04.2026

10 Min Read

TL;DR

European technology M&A activity in Q4 2025 was driven by enterprise AI infrastructure, cybersecurity consolidation, and sovereign semiconductor development. The largest potential transaction involved ServiceNow’s planned $7.75B acquisition of Armis, strengthening its enterprise security ecosystem. Other notable deals include Workday acquiring Sana for $1.1B to expand AI-powered HR platforms and Qualcomm purchasing Ventana Micro to accelerate RISC-V chip design. These transactions highlight Europe’s strategic push toward AI-ready enterprise platforms and greater technological sovereignty in semiconductor architecture.

Mini-Glossary

RISC-V Architecture

An open-source processor instruction set architecture that allows companies to design custom chips without licensing proprietary architectures such as ARM.

Identity Governance and Administration (IGA)

Security systems that manage and audit user permissions across enterprise software environments.

AI Security

Cybersecurity technologies designed to protect artificial intelligence systems from threats such as data poisoning, prompt injection, or model manipulation.

Enterprise AI Platform

Integrated infrastructure that combines data pipelines, AI models, analytics tools, and security layers for enterprise applications.

Operational Technology (OT)

Industrial systems such as manufacturing equipment, sensors, and connected infrastructure that require specialized cybersecurity protection.

Key Deals

Deal Rationale

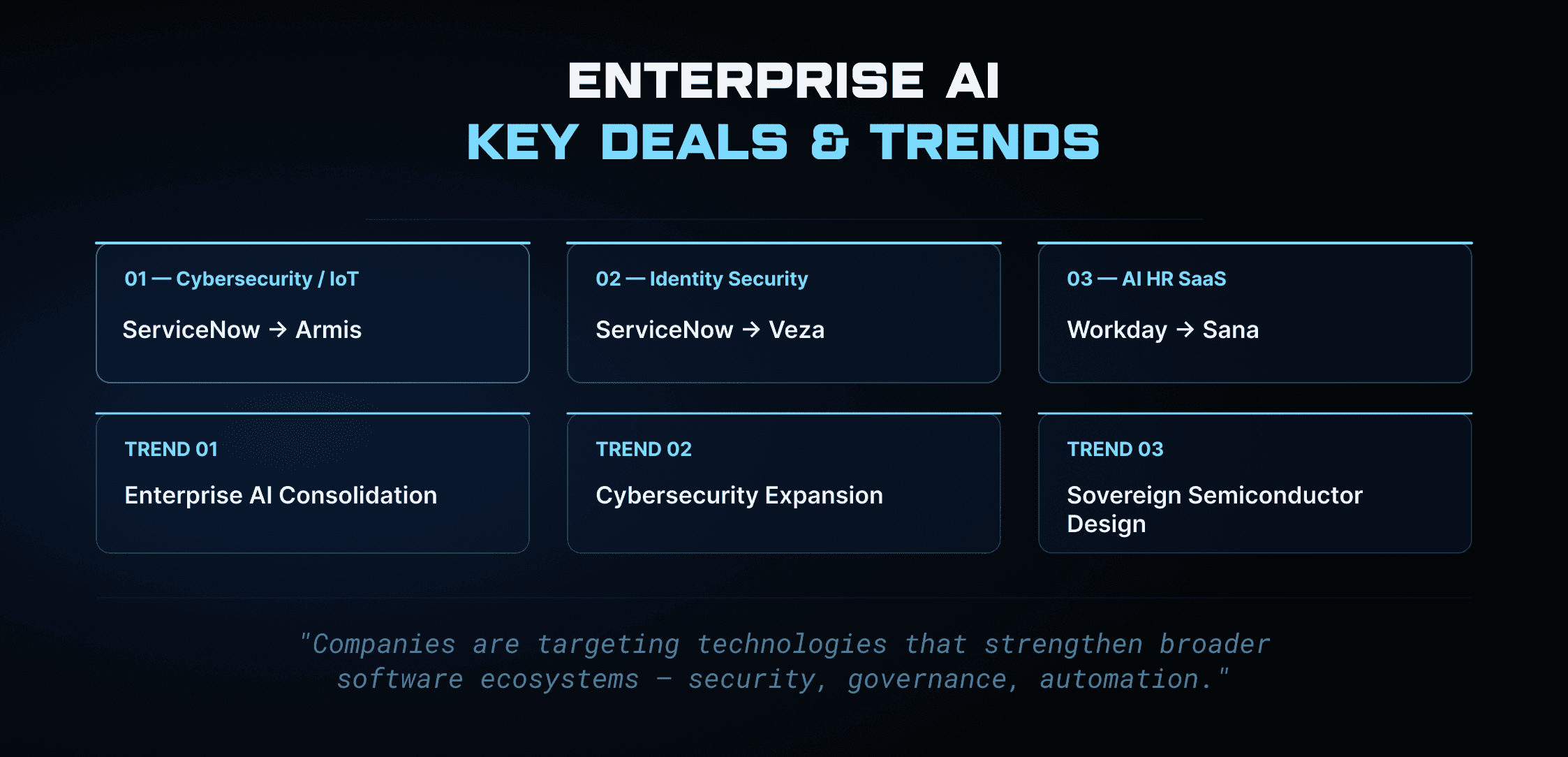

Technology M&A activity in Europe during Q4 2025 was largely focused on building integrated enterprise AI ecosystems.

ServiceNow’s planned acquisitions of Armis and Veza illustrate this strategy. Armis provides enterprise-wide asset visibility across IoT and operational technology environments, while Veza focuses on identity governance. Together, these platforms could allow ServiceNow to provide a unified enterprise security architecture.

In the consulting space, Accenture’s acquisition of Decho strengthens its AI deployment capabilities, particularly for enterprise clients implementing large-scale analytics and automation platforms.

The semiconductor sector also saw strategic investment. Qualcomm’s purchase of Ventana Micro reflects growing global interest in RISC-V chip architecture, which enables companies to develop custom processors without relying on proprietary designs.

Finally, Workday’s acquisition of Sana demonstrates how enterprise software providers are integrating AI assistants into workplace platforms to automate knowledge management and employee support.

Market Trends

Several trends defined the European technology M&A environment in Q4 2025.

Enterprise AI Platform Consolidation

Large enterprise software providers are building full-stack AI platforms by integrating data infrastructure, security systems, and application layers.

Cybersecurity Expansion

As enterprise IT environments grow more complex, companies increasingly acquire specialized security firms to protect cloud, IoT, and AI systems.

Sovereign Semiconductor Design

European technology companies are investing in alternative chip architectures such as RISC-V to reduce dependency on proprietary processor technologies.

These developments indicate that technology companies are moving toward platform-driven M&A strategies, where acquisitions support the creation of integrated enterprise ecosystems.

Structured Signals

Signal Card | Description | Context | Confidence |

SAP ESG adoption | Data compliance tools integrated with S/4HANA | German Mittelstand companies | Medium |

Nordic 6G initiatives | Early infrastructure and network experiments | Scandinavian telecom-tech partnerships | Medium |

AI governance tools | Enterprise compliance software for AI systems | EU regulatory environment | Medium |

Analyst Thesis

European technology M&A is increasingly focused on building integrated AI infrastructure for enterprises.

Rather than acquiring standalone products, companies are targeting technologies that strengthen broader software ecosystems, including cybersecurity, data governance, and automation platforms.

The growing adoption of RISC-V architecture also reflects geopolitical concerns around technology supply chains. By investing in open processor architectures, companies can develop greater independence in chip design while still relying on global manufacturing networks.

Meanwhile, enterprise demand for AI-driven automation continues to grow rapidly, pushing software vendors to integrate AI agents directly into business workflows.

Looking ahead, the next wave of technology acquisitions in Europe will likely focus on AI governance, data infrastructure, and enterprise automation platforms.

What Changed in Q4 2025

Enterprise software vendors accelerated acquisitions related to AI infrastructure and cybersecurity.

Open processor architectures such as RISC-V gained strategic importance.

AI assistants began integrating directly into enterprise software platforms.

Sources Hierarchy

Tier 1 — Primary sources

Corporate announcements, investor presentations, regulatory filings.

Tier 2 — Financial media

Bloomberg, Reuters, Financial Times.

Tier 3 — Industry data platforms

PitchBook, Crunchbase, venture capital research databases.

Confidence Framework

High Confidence

Confirmed transactions or officially announced deals.

Medium Confidence

Deals reported by reputable financial media but still in negotiation stages.

Low Confidence

Early-stage discussions or speculative market signals.

FAQ

What were the largest tech M&A deals in Europe in Q4 2025?

Notable deals include ServiceNow’s planned $7.75B acquisition of Armis, Workday purchasing Sana for $1.1B, and Qualcomm acquiring Ventana Micro to expand RISC-V chip development.

Why are cybersecurity companies frequent acquisition targets?

As enterprise IT systems become more interconnected, cybersecurity tools are increasingly integrated into broader enterprise software platforms.

Why is RISC-V important for the European technology sector?

RISC-V allows companies to design custom processors without relying on proprietary architectures, helping support technological sovereignty and innovation in chip design.

How is AI influencing enterprise software acquisitions?

Companies are acquiring technologies that support AI automation, knowledge management, and advanced data analytics, integrating these capabilities directly into enterprise platforms.