Vlad Zghurskyi

01.04.2026

10 Min Read

TL;DR

European defense and dual-use technology M&A in Q4 2025 accelerated as governments increased military spending and prioritized sovereign defense capabilities. Key transactions included Helsing’s acquisition of Grob Aircraft’s military division and Safran Electronics & Defense acquiring Preligens, a French AI defense analytics company. At the same time, venture-backed startups across drone systems, AI battlefield software, and satellite intelligence attracted significant strategic investment. The sector is moving toward AI-driven warfare systems, autonomous platforms, and defense software integration, creating a new generation of dual-use defense technology companies in Europe.

Mini-Glossary

Dual-Use Technology

Technologies that can be used for both civilian and military purposes, such as AI analytics, satellite imaging, or drone navigation systems.

ISR (Intelligence, Surveillance, Reconnaissance)

Systems designed to collect battlefield intelligence using satellites, drones, sensors, and analytics platforms.

Autonomous Systems

Weapons or military platforms capable of performing operations with limited human control, including drones and robotic vehicles.

Electronic Warfare (EW)

Military technologies used to disrupt, jam, or manipulate enemy communications and radar systems.

Loitering Munitions

Drones that remain airborne while searching for targets before striking them.

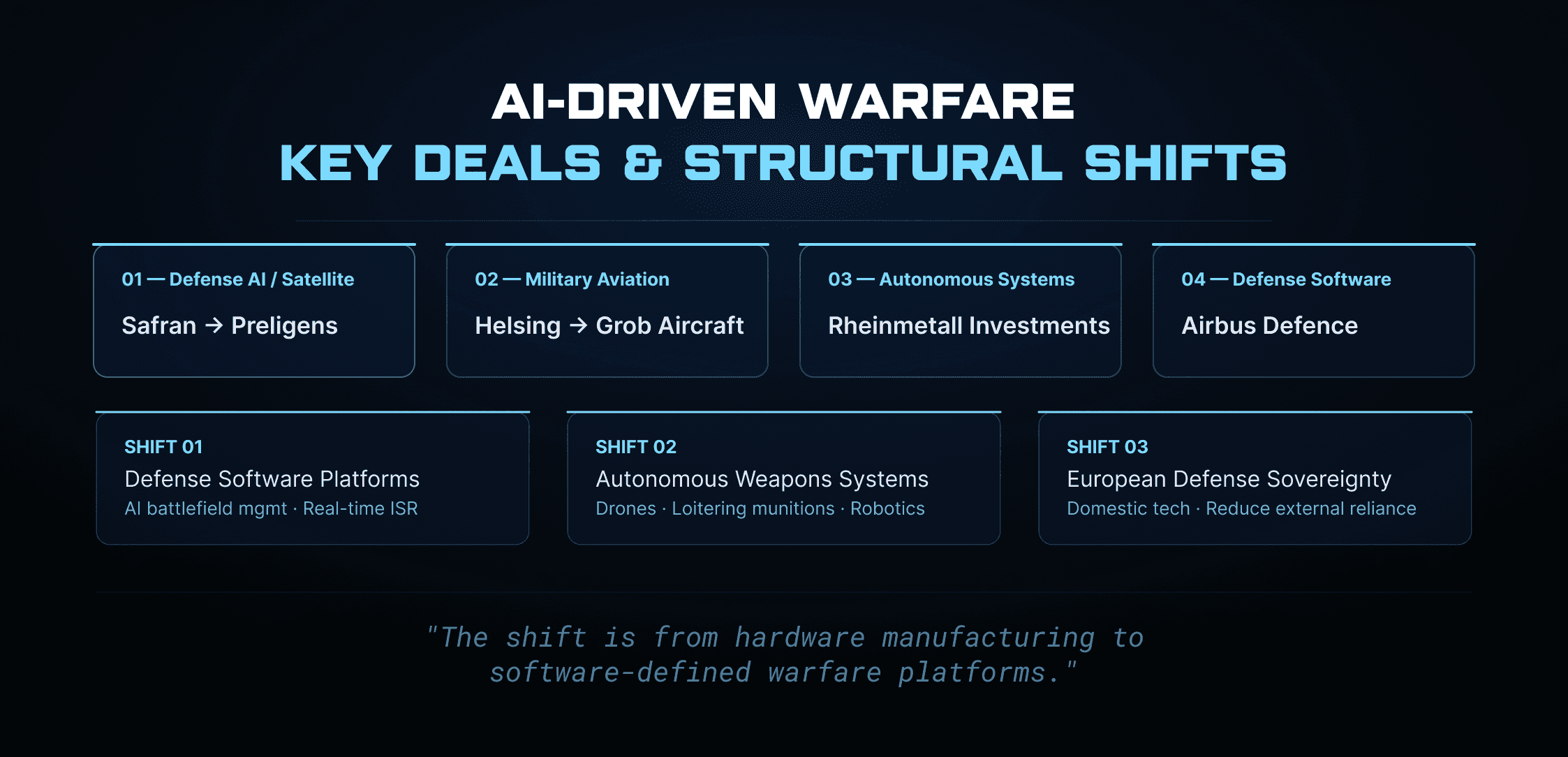

Key Deals

Deal Rationale

European defense technology acquisitions are increasingly focused on software, AI analytics, and autonomous systems rather than traditional hardware manufacturing.

The acquisition of Preligens by Safran Electronics & Defense highlights the importance of AI-driven intelligence analysis. Preligens specializes in machine-learning software capable of automatically detecting military assets in satellite imagery, dramatically accelerating intelligence workflows.

Meanwhile, Helsing’s purchase of Grob Aircraft’s military division represents a strategic move to combine AI defense software with aircraft platforms, enabling the development of autonomous or semi-autonomous defense systems.

Defense contractor Rheinmetall has also expanded its investments in drone manufacturers and robotics firms as European armies rapidly adopt unmanned battlefield systems.

These transactions reflect a shift in defense industry priorities from pure hardware manufacturing to software-defined warfare platforms.

Market Trends

Several structural trends are shaping the European defense technology M&A landscape.

Defense Software Platforms

AI-powered battlefield management systems are becoming a major investment theme as military operations increasingly rely on real-time data analysis.

Autonomous Weapons Systems

Drones, robotic vehicles, and loitering munitions are transforming battlefield strategy, creating demand for startups capable of developing autonomous systems.

European Defense Sovereignty

Governments across Europe are encouraging domestic defense technology development to reduce reliance on external suppliers and improve strategic autonomy.

Structured Signals

Signal Card | Description | Context | Confidence |

NATO defense spending increase | Member states raising military budgets | Post-Ukraine war security strategy | High |

European drone startup funding | Venture capital entering defense sector | Ukraine battlefield innovation | High |

AI battlefield analytics adoption | Military adoption of automated intelligence systems | Satellite and sensor data analysis | Medium |

Analyst Thesis

European defense technology is undergoing a structural transformation toward software-defined military systems.

Traditional defense contractors are increasingly acquiring AI startups, drone manufacturers, and analytics companies to integrate advanced digital capabilities into existing platforms. This shift is driven by recent conflicts demonstrating the strategic importance of autonomous systems, satellite intelligence, and battlefield data analytics.

Another major driver is the push for European defense sovereignty. Governments are actively supporting domestic defense technology companies to reduce reliance on external suppliers, particularly in sensitive areas such as surveillance, electronic warfare, and autonomous weapons.

As a result, the European defense technology ecosystem is expected to see continued consolidation between startups and established defense contractors, with AI and drone technologies remaining key acquisition targets.

What Changed in Q4 2025

AI-powered intelligence platforms became major acquisition targets.

Defense contractors increased investments in autonomous systems and drone technologies.

European governments accelerated funding for domestic defense innovation.

Sources Hierarchy

Tier 1 — Primary sources

Defense company announcements, government procurement disclosures, regulatory filings.

Tier 2 — Financial media

Reuters, Bloomberg, Financial Times.

Tier 3 — Defense industry research

Defense News, SIPRI, venture capital databases.

Confidence Framework

High Confidence

Confirmed deals or officially announced acquisitions.

Medium Confidence

Reported by reputable media or supported by multiple industry sources.

Low Confidence Early-stage investments or strategic partnership signals.

FAQ

Why is defense technology M&A increasing in Europe?

Rising geopolitical tensions and increased military budgets have pushed European governments and defense contractors to invest heavily in advanced military technologies.

What types of companies are being acquired?

The most common targets are AI analytics startups, drone manufacturers, satellite intelligence companies, and defense software developers.

Why are autonomous systems important in modern defense?

Autonomous systems reduce operational risk, improve battlefield intelligence collection, and allow military forces to operate effectively in contested environments.